How are closing entries done?

.

Subsequently, one may also ask, how are closing entries done in accounting?

Closing entries, also called closing journal entries, are entries made at the end of an accounting period to zero out all temporary accounts and transfer their balances to permanent accounts. In other words, the temporary accounts are closed or reset at the end of the year.

Beside above, what are closing entries Why are they needed? The Purpose of Closing Entries A term often used for closing entries is "reconciling" the company's accounts. Accountants perform closing entries to return the revenue, expense, and drawing temporary account balances to zero in preparation for the new accounting period.

Accordingly, how do you write a closing entry example?

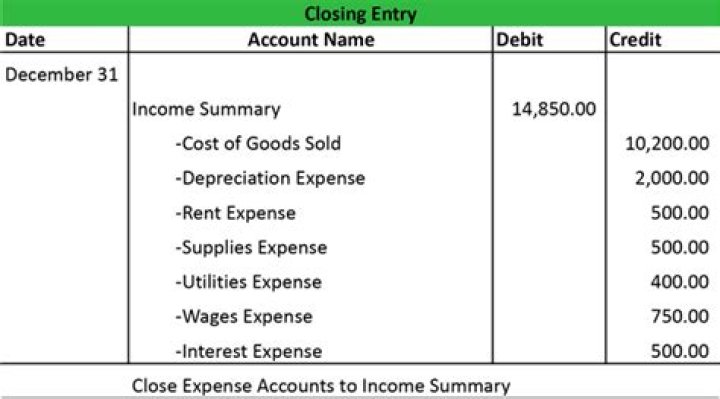

Example of a Closing Entry

- Close Revenue Accounts. Clear the balance of the revenue.

- Close Expense Accounts. Clear the balance of the expense accounts by debiting income summary and crediting the corresponding expenses.

- Close Income Summary.

- Close Dividends.

What are the 4 closing entries?

The four basic steps in the closing process are: Closing the revenue accounts—transferring the credit balances in the revenue accounts to a clearing account called Income Summary. Closing the expense accounts—transferring the debit balances in the expense accounts to a clearing account called Income Summary.

Related Question AnswersWhat are closing journal entries?

Closing entries are journal entries made at the end of an accounting period which transfer the balances of temporary accounts to permanent accounts. Closing entries are based on the account balances in an adjusted trial balance. Revenue, Income and Gain Accounts. Expense and Loss Accounts.What happens if closing entries are not made?

Without completing such closing entries, a company's income statement accounts are not ready to record revenue and expense transactions for the next accounting period, and the amount of retained earnings is not correctly stated, causing the balance sheet to be unbalanced.What is an adjusting journal entry?

An adjusting journal entry is an entry in a company's general ledger that occurs at the end of an accounting period to record any unrecognized income or expenses for the period. Adjusting journal entries can also refer to financial reporting that corrects a mistake made previously in the accounting period.How many closing entries are there?

four closing entriesWhat is the difference between adjusting and closing entries?

In addition, the adjustments tend to be forced upon the accountant because the accounting cycle is coming to an end and the financial statements need to be prepared. Closing entries occur at the end of the accounting cycle as well. These entries are made in order to prepare for a new accounting cycle.Why temporary accounts are closed each period?

Temporary accounts refer to accounts that are closed at the end of every accounting period. These accounts include revenue, expense, and withdrawal accounts. They are closed to prevent their balances from being mixed with those of the next period.What accounts are closed in the closing entries?

Only revenue, expense, and dividend accounts are closed—not asset, liability, Common Stock, or Retained Earnings accounts. The four basic steps in the closing process are: Closing the revenue accounts—transferring the credit balances in the revenue accounts to a clearing account called Income Summary.What is an opening entry?

An opening entry is the initial entry used to record the transactions occurring at the start of an organization. The contents of the opening entry typically include the initial funding for the firm, as well as any initial debts incurred and assets acquired.Is Income Summary a debit or credit?

Next, if the Income Summary has a credit balance, the amount is the company's net income. If the Income Summary has a debit balance, the amount is the company's net loss. The Income Summary will be closed with a credit for that amount and a debit to Retained Earnings or the owner's capital account.What is the purpose of closing entries quizlet?

Closing entries are journal entries used to empty temporary accounts at the end of a reporting period and transfer their balances into permanent accounts.How do you close the books in accounting?

- 8 Steps to Close the Books. Closing the books is a process usually performed by an accountant.

- Transfer Journal Entries to the General Ledger.

- Sum the General Ledger Accounts.

- Make a Preliminary Trial Balance.

- Enter Adjusting Journal Entries.

- Make an Adjusted Trial Balance.

- Generate Financial Statements.

- Enter Closing Entries.

What is adjusting entries in accounting with example?

These are revenues received in advance and recorded as liabilities, to be recorded as revenue and expenses paid in advance and recorded as assets, to be recorded as expense. For example, adjustments to unearned revenue, prepaid insurance, office supplies, prepaid rent, etc.What accounts are affected by closing entries What accounts are not affected?

What accounts are affected by closing entries? What accounts are not affected? Revenues, Expenses, dividends, and income summary accounts were affected. Assets, liabilities, and retained earnings are not affected.How do you do month end closing?

Month-end closing process- Record incoming cash. When closing your books monthly, you need to record the funds you received during the month.

- Update accounts payable.

- Reconcile accounts.

- Review petty cash.

- Look at fixed assets.

- Count inventory.

- Organize and review financial statements.

- Check revenue and expense accounts.