How do you calculate Fama French factors

The Fama-French Three Factor model is a formula for calculating the likely return on a stock market investment. It measures this return based on a comparison of the investment to the overall risk in the market, the size of the companies involved and their book-to-market values (the inverse of the price-to-book ratio).

How are the Fama French factors calculated?

The Fama-French Three Factor model is a formula for calculating the likely return on a stock market investment. It measures this return based on a comparison of the investment to the overall risk in the market, the size of the companies involved and their book-to-market values (the inverse of the price-to-book ratio).

How do you do Fama in French?

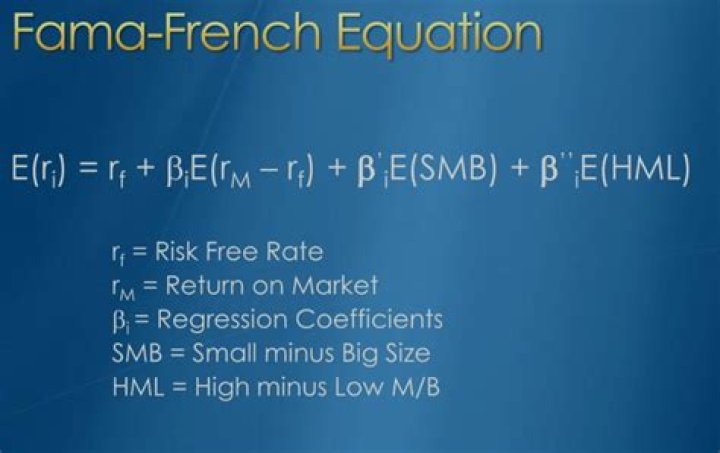

- r = Expected rate of return.

- rf = Risk-free rate.

- ß = Factor’s coefficient (sensitivity)

- (rm – rf) = Market risk premium.

- SMB (Small Minus Big) = Historic excess returns of small-cap companies over large-cap companies.

How do you do the Fama French three factor model?

- Calculate the average 1 month return, 2 month return,, 3 month return, …. …

- Calculate the 1 month average, 2 month average, 3 month average, …. …

- Subtract 1 month average Rf from average 1 month return, repeat until the 36th month.

What are the 5 factors in Fama French?

The empirical tests of the five-factor model aim to explain average returns on portfolios formed to produce large spreads in Size, B/M, profitability and investment. Firstly, the model is applied to portfolios formed on size, B/M, profitability and investment.

What are the Fama and French 3 factors?

The Fama and French model has three factors: the size of firms, book-to-market values, and excess return on the market. In other words, the three factors used are SMB (small minus big), HML (high minus low), and the portfolio’s return less the risk-free rate of return.

What is the Fama French 4 Factor Model?

Today, the four factors of market, style, size, and momentum, constitute the Fama-French 4 Factor Model.

How does Fama MacBeth regression work?

The Fama–MacBeth regression is a method used to estimate parameters for asset pricing models such as the capital asset pricing model (CAPM). … Then regress all asset returns for each of T time periods against the previously estimated betas to determine the risk premium for each factor.How do you make a Fama French portfolio?

The Fama-French Portfolios are constructed from the intersections of two portfolios formed on size, as measured by market equity (ME), and three portfolios using the ratio of book equity to market equity (BE/ME) as a proxy for value.

What is Fama and French 5 factor model?The Fama/French 5 factors (2×3) are constructed using the 6 value-weight portfolios formed on size and book-to-market, the 6 value-weight portfolios formed on size and operating profitability, and the 6 value-weight portfolios formed on size and investment.

Article first time published onAre the Fama and French factors global or country specific Griffin?

Griffin (2002) demonstrates that the performance of Fama-French country-specific factor regression is much better than global-factor model, whereas Blanco (2012) shows that its expected outcome depends upon how the stock portfolios are formed (e.g. based on characteristics relating to risk factors).

Is the Fama French three factor model better than the CAPM?

Empirical results point out that Fama and French Three Factor Model is better than CAPM according to the goal of explaining the expected returns of the portfolios.

What is Fama French momentum factor?

The Fama-French model, developed in the 1990, argued most stock market returns are explained by three factors: risk, price (value stocks tending to outperform) and company size (smaller company stocks tending to outperform). Carhart added a momentum factor for asset pricing of stocks.

Why is Fama French better than CAPM?

CAPM has been prevalently used by practitioners for calculating required rate of return despite having drawbacks. … It means that Fama French model is better predicting variation in excess return over Rf than CAPM for all the five companies of the Cement industry over the period of ten years.

How do you calculate WML?

The WML factor is computed as the difference between the average of returns on winners portfolios (SW as well as BW) and losers portfolios (SL and BL).

What is Fama?

noun. fame [noun] the quality of being well-known. name [noun] reputation; fame.

What is beta in Fama French?

Fama-French Market Beta is the beta used for the Market Risk Premium (CAPM also uses a Market Risk Premium Beta, but the FF Market Beta and CAPM Beta are not interchangeable, as CAPM uses a single beta for expected returns, whereas Fama-French uses three betas.)

What is the distribution of stock returns suggested by Fama and French?

Rubinstein (1973) derives an equation for the expected return in terms of an arbitrary number of co-moments. We test whether SMB and HML proxy for these co-moments.

How are the SMB and HML factors constructed?

To construct the SMB and HML factors, we sort stocks in a region into two market cap and three book-to-market equity (B/M) groups at the end of each June. Big stocks are those in the top 90% of June market cap for the region, and small stocks are those in the bottom 10%.

How do you calculate alpha?

- Alpha = Actual Rate of Return – Expected Rate of Return. …

- Expected Rate of Return = Risk-Free Rate + β * Market Risk Premium. …

- Alpha = Actual Rate of Return – Risk-Free Rate – β * Market Risk Premium.

What does the Jensen alpha measure?

The Jensen’s measure, or Jensen’s alpha, is a risk-adjusted performance measure that represents the average return on a portfolio or investment, above or below that predicted by the capital asset pricing model (CAPM), given the portfolio’s or investment’s beta and the average market return.

Is Fama MacBeth regression a cross sectional regression or time series regression?

We use the cross-section regression approach of Fama and MacBeth (1973) to construct cross-section factors corresponding to the time-series factors of Fama and French (2015).

What is UMD in Fama French?

Momentum (UMD) – The return of the equal weighted average of the 50% highest performing stocks minus the return of the equal weighted average of the 50% lowest performing stocks. The momentum factor is a bit controversial in that there are convincing risk-based as well as behavioral-based explanations.

What is a major criticism of Fama and French model?

One of the major criticisms of the Fama French model was that the value premium was sample specific and was likely to be a “mere artifact of data mining” as indicated by Black (1993). Black (1993) argued that the existence of value premium is a mere chance unlikely to recur in future returns.

How is apt different from CAPM?

2 Unlike the CAPM, the APT does not indicate the identity or even the number of risk factors. … While the CAPM formula requires the input of the expected market return, the APT formula uses an asset’s expected rate of return and the risk premium of multiple macroeconomic factors.

What is CMA Fama-French?

Defined analogously to the HML factor, the profitability factor (RMW) is the difference between the returns of firms with robust (high) and weak (low) operating profitability; and the investment factor (CMA) is the difference between the returns of firms that invest conservatively and firms that invest aggressively.

Does Fama-French still work?

Although the Fama-French factors still show a strong long-term performance, they have now experienced two lost decades during which various other factors were able to deliver. … Fama-French factors are considered a standard in academic research and their definitions are widely used in empirical studies.