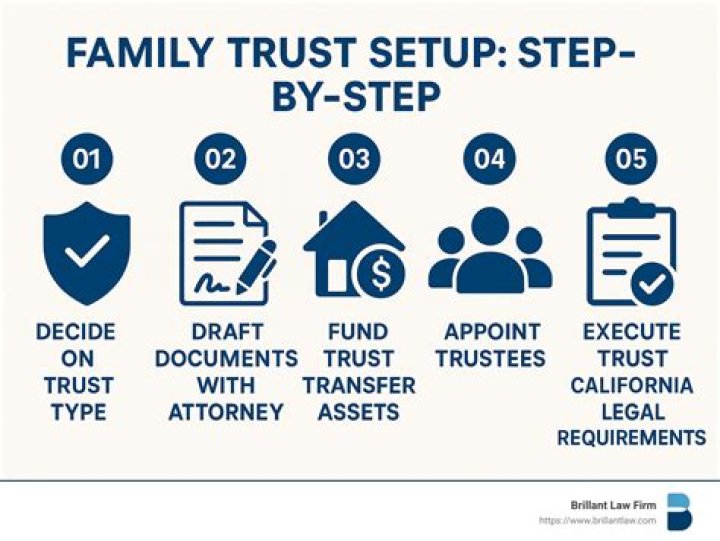

How do you set up a family trust?

- Write down the assets you want to include in thetrust.

- Select a trustee.

- Make a list of beneficiaries.

- Write down the trust's distribution rules.

- Write down the goal of the trust and what benefits youwant to receive.

- Select a trust name.

- Contact an estate attorney.

- Check over the proposed trust agreement.

.

Also question is, what is the point of a family trust?

A family trust is a trust establishedspecifically for the benefit of members of a particularfamily. The purpose of creating a family trustis to protect and manage family assets for current and / orfuture generations.

Likewise, why would a person want to set up a trust? Trusts can help pass and preserve wealthefficiently and privately. Trusts can help reduce estatetaxes for married couples. Gain control over distribution of yourassets by using trusts. With a trust, you canensure that your retirement assets are distributed as you'veplanned.

Correspondingly, how much does it cost to set up a trust?

Attorney's fees are generally the bulk of thecost associated with creating a trust. Thecost for an attorney to draft a living trust canrange from $1,000 to $1,500 for individuals and $1,200 to $2,500for married couples.

What do you need to set up a trust?

Steps to Set Up a Living Trust:

- Decide whether you need a shared trust or an individualtrust.

- Decide what items to leave in the trust.

- Decide who will inherit your trust property.

- Choose someone to be your successor trustee.

- Choose someone to manage property for youngsters.

- Prepare the trust document.

What are the disadvantages of a trust?

The Disadvantages of a Living Trust- Characteristics of a Trust. A living trust allows someone totransfer legal ownership of assets to a trustee.

- Expense. One of the primary drawbacks to using a trust is thecost necessary to establish it.

- More Details. Trusts are often much more complex to draftcompared to wills.

- Lack of Tax Advantages.

- Inconvenience.

Who owns the property in a trust?

To create a trust, the property owner(called the "trustor," "grantor," or "settlor") transfers legalownership to a person or institution (called the "trustee")to manage that property for the benefit of another person(called the "beneficiary").Who controls a family trust?

Who controls a family trust?“Appointor” is the term used in many discretionaryfamily trust deeds to describe the person who has the powerto appoint and remove the trustee.Can a trustee withdraw money from a trust?

Trustees Can Withdraw For TrustUse Trust law varies from state to state, but underno circumstances can a trustee withdraw funds from thetrust for the personal use of the trustee. Commontrust law dictates that the trustee (or trustees) arethe only parties that can disburse funds from a trustaccount.Do family trusts pay tax?

Family Trust income They do not have to make trustdistributions in any particular proportion or in the sameproportions as they did in previous years. A trustdoes not have to pay income tax on income that isdistributed to the beneficiaries, but does have to paytax on undistributed income.Can family trust buy property?

A family discretionary trust is probablythe most common type of trust for property investors.The trustee can use their discretion to distribute thetrust's income and assets to the beneficiaries, allowing thefamily members to take advantage of taxbenefits.Why would you create a trust?

Once you place assets in the trust, theyare no longer yours. A trustee is a bank, attorney orother entity set up for this purpose. Since the assetsare no longer yours, you don't have to payincome tax on any money made from the assets. Also, with properplanning, the assets can be exempt from estate and gifttaxes.When should I set up a family trust?

An irrevocable family trust has the same benefits as arevocable trust, but has the possible additional benefitsof:- Protecting assets from creditors.

- Avoiding estate taxes.

- Helping enable qualification for Medicaid benefits, in theevent the grantor requires skilled nursing care.

How much money is usually in a trust fund?

Less than 2 percent of the U.S. population receives atrust fund, usually as a means of inheriting largesums of money from wealthy parents, according to the Surveyof Consumer Finances. The median amount is about $285,000 (theaverage was $4,062,918) — enough to make a major, lastingimpact.Do you need a lawyer to create a trust?

When you create a DIY living trust, thereare no attorneys involved in the process. It is also possible tochoose a company, such as a bank or a trust company, to beyour trustee. You'll also need to choose yourbeneficiary or beneficiaries, the person or people who will receivethe assets in your trust.Is it better to have a will or a trust?

A trust passes outside of probate, so a courtdoes not need to oversee the process, which can save time andmoney. Unlike a will, which becomes part of the publicrecord, a trust can remain private. Wills and trustseach have their advantages and disadvantages.Does a trustee own the property?

A trustee is responsible for managing theproperty owned by a trust for the benefit of the trustbeneficiaries. His exact duties can vary based on what assets thetrust owns.Why use a trust instead of a will?

Avoiding the cost of probate is often a factor whenchoosing a living trust, but many people are just asinterested in avoiding the court process altogether, along with itsdelays, lack of privacy, loss of control and emotional stress. Aproperly prepared and funded living trust avoids courtinterference at incapacity.What are the benefits of a trust?

Among the chief advantages of trusts, they letyou:- Put conditions on how and when your assets are distributedafter you die;

- Reduce estate and gift taxes;

- Distribute assets to heirs efficiently without the cost, delayand publicity of probate court.

- Better protect your assets from creditors and lawsuits;

Should I put my house in a trust?

The main reason individuals put their home in aliving trust is to avoid the costly and lengthy probateprocess at death. Since you can access the assets in thetrust at any time, a revocable trust does not provideasset protection from creditors or remove the home from yourtaxable estate at death.Why do I need a trust bank account?

Most banks offer trust accounts as anoptional service. In a trust account, a trusteecontrols funds for the benefit of another party - an individual ora group.The bank trust account is a useful way to convey andcontrol assets on behalf of a third-party owner.Can I put my house in a trust to avoid care home fees?

“If you had put your property intotrust before going into care, then thestarting point is that it is no longer owned by you. Yourhome is not part of your capital and you cannot berequired to use it to fund your care fees.Is there a yearly fee for a trust?

Typically, professional trustees, such as banks,trust companies, and some law firms, charge between1.0% and 1.5% of trust assets per year, depending inpart on the size of the trust. A trust holding$200,000 and paying a fee of 1.5% would pay an annualfee of $3,000, which may or may not cover the trustee'scosts.What should you not put in a living trust?

What Assets Can Go Into a Revocable Living Trust?- Cash Accounts. Rafe Swan / Getty Images.

- Non-Retirement Investment and Brokerage Accounts. leezsnow /Getty Images.

- Nonqualified Annuities. Westend61 / Getty Images.

- Stocks and Bonds Held in Certificate Form. Tetra Images / GettyImages.

- Tangible Personal Property.

- Business Interests.

- Life Insurance.

- Monies Owed to You.