The collective decisions passed down from the APB and FASB form GAAP. The American Institute of Certified Public Accountants (AICPA), the SEC, and the Governmental Accounting Standards Board (GASB), are the core organizations that influence GAAP in addition to the FASB..

Similarly, what organizations influence GAAP explain how they do so?

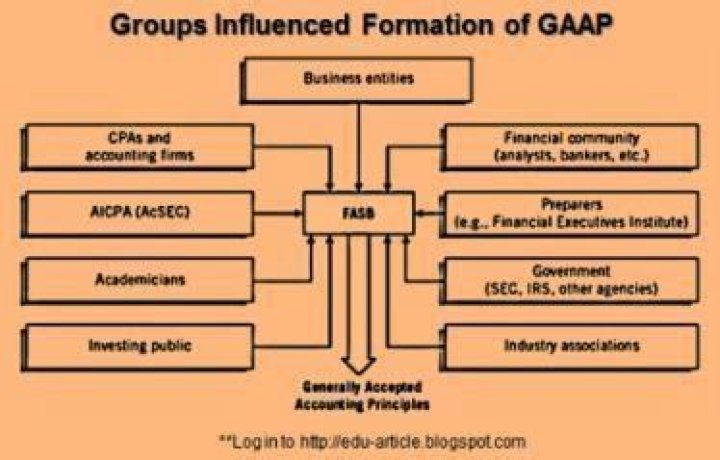

In the U.S., several organizations influence what GAAP rules, including the Financial Accounting Standards Board (FASB), the American Institute of Certified Public Accountants (AICPA), the Securities and Exchange Commission (SEC), and the Internal Revenue Service (IRS).

One may also ask, what are the 4 principles of GAAP? The four basic constraints associated with GAAP include objectivity, materiality, consistency and prudence.

Likewise, are all companies required to follow GAAP?

Not all businesses are required to follow GAAP. The U.S. Securities and Exchange Commission (SEC) requires publicly traded companies to follow GAAP in addition to other SEC rules. If you are preparing financial statements to secure outside funding, you must follow generally accepted accounting principles.

Who writes GAAP rules?

The phrase "generally accepted accounting principles" (or "GAAP") consists of three important sets of rules: (1) the basic accounting principles and guidelines, (2) the detailed rules and standards issued by FASB and its predecessor the Accounting Principles Board (APB), and (3) the generally accepted industry

Related Question Answers

Is GAAP going away?

Had the anticipated move come about, U.S. Generally Accepted Accounting Principles (GAAP) would have been abandoned. The switch, however, never happened. Now SEC Chairman Jay Clayton has announced that a consideration to require or allow U.S. public companies to use IFRS is “not a focus” for him.When was GAAP formed?

1973

What are GAAP rules?

Generally accepted accounting principles, or GAAP, are a set of rules that encompass the details, complexities, and legalities of business and corporate accounting. The Financial Accounting Standards Board (FASB) uses GAAP as the foundation for its comprehensive set of approved accounting methods and practices.Why is GAAP necessary?

GAAP allows investors to easily evaluate companies simply by reviewing their financial statements. When applied to government entities, GAAP helps taxpayers understand how their tax dollars are being spent. GAAP also helps companies gain key insights into their own practices and performance.What is GAAP comprised of?

true. GAAP stands for: Generally Accepted Accounting Principles. Before the codification, GAAP was comprised of: FASB standards, interpretations, ETIF consensus, and accounting rules issued by FASB predecessor organizations.Is GAAP a law?

GAAP is not law, and there is nothing illegal about violations of its rules unless those violations happen to coincide with other laws. Certified Public Accountants (CPAs) must be hired to audit accounting records and financial statements for publicly traded companies to ensure their conformity with GAAP.What are the advantages of GAAP?

GAAP guidelines help businesses maintain consistency in their presentation of financial information, reduce the risk of misrepresentation and avoid fraud. GAAP was created to safeguard the rights of stakeholders, including investors.What are the 5 basic accounting principles?

5 principles of accounting are; - Revenue Recognition Principle,

- Historical Cost Principle,

- Matching Principle,

- Full Disclosure Principle, and.

- Objectivity Principle.

Why do most companies adhere to GAAP?

Why do most companies adhere to GAAP for their basic internal financial statements? A. GAAP is required by law for publicly held companies. Accrual accounting provides a uniform method to measure an organization's financial performance.Who is subject to GAAP?

The Principles of GAAP Generally accepted accounting principles, or GAAP for short, are the accounting rules used to prepare and standardize the reporting of financial statements, such as balance sheets, income statements and cashflow statements, for publicly traded companies and many private companies in the UnitedDo all companies have to use GAAP?

The U.S. Securities and Exchange Commission (SEC) requires publicly traded companies to follow GAAP in addition to other SEC rules. Small, private companies are generally not required to use GAAP because many of the rules do not apply. And, GAAP requires that you use accrual accounting.Do private companies have to use GAAP?

Both private and public companies are subject to generally accepted accounting principles (GAAP), although for different reasons. The SEC requires publicly traded companies to provide GAAP-compliant audited financial statements. However, many private companies don't issue audited financial statements.What is the difference between GAAP and IFRS?

The primary difference between the two systems is that GAAP is rules-based and IFRS is principles-based. GAAP does not allow for inventory reversals, while IFRS permits them under certain conditions. Another key difference is that GAAP requires financial statements to include a statement of comprehensive income.What happens if you violate GAAP?

Errors or omissions in applying GAAP can be costly in a business transaction; impacting credibility with lenders and leading to incorrect decisions. These violations can cause inaccurate reporting for internal and budgeting purposes, as well as a reduced reliance on prepared financial statements for 3rd party readers.Is GAAP and FASB the same?

These common standards are better known as GAAP. The term GAAP stands for Generally Accepted Accounting Principles; which are the guiding rules and standards that have been set by the Financial Accounting Standards Board (FASB), and adopted by the United States accounting profession as a whole.What are accounting procedures?

An accounting procedure is a standardized process that is used to perform a function within the accounting department. Examples of accounting procedures are: Issue billings to customers. Pay invoices from suppliers. Calculate payroll for employees.Who is the father of accounting?

Luca Pacioli

What is debit and credit?

A debit is an accounting entry that either increases an asset or expense account, or decreases a liability or equity account. It is positioned to the left in an accounting entry. A credit is an accounting entry that either increases a liability or equity account, or decreases an asset or expense account.What are the 3 types of accounting?

There are mainly three types of accounts in accounting: Real, Personal and Nominal accounts, personal accounts are classified into three subcategories: Artificial, Natural, and Representative.