What percentage of mortgages are subprime

The percentage of lower-quality subprime mortgages originated during a given year rose from the historical 8% or lower range to approximately 20% from 2004 to 2006, with much higher ratios in some parts of the U.S. A high percentage of these subprime mortgages, over 90% in 2006 for example, had an interest rate that …

What percentage of mortgages were subprime?

Around 33 percent of all borrowers (not just of mortgages) fall into the subprime category based on credit score, according to Experian.

What type of people get subprime mortgages?

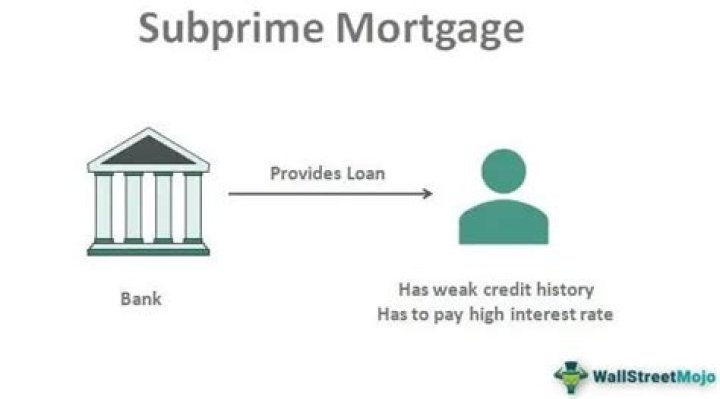

A subprime mortgage is a type of loan granted to individuals with poor credit scores who wouldn’t qualify for conventional mortgages. Subprime mortgages are now making a comeback as nonprime mortgages.

How large is the subprime market?

The market size, measured by revenue, of the Subprime Auto Loans industry is $14.4bn in 2021. What is the growth rate of the Subprime Auto Loans industry in the US in 2021?Is subprime mortgage high risk?

Because subprime borrowers are riskier, they carry higher interest rates than prime loans. The specific amount of interest charged on a subprime loan is not set in stone. Different lenders may not evaluate a borrower’s risk in the same manner.

What percentage of mortgages were subprime in 2007?

Between 2004 and 2006 the share of subprime mortgages relative to total originations ranged from 18%–21%, versus less than 10% in 2001–2003 and during 2007.

Why were there so many subprime mortgages?

The subprime mortgage crisis of 2007–10 stemmed from an earlier expansion of mortgage credit, including to borrowers who previously would have had difficulty getting mortgages, which both contributed to and was facilitated by rapidly rising home prices.

Why were homeowners willing to take out mortgages that they could not afford?

However, it is true that many subprime borrowers willfully took on mortgages that they would probably not be able to pay off because they knew that if they were ever unable to make their mortgage payments, they would be able to sell their house for a profit in the growing housing market.Were banks forced to make subprime loans?

Several candidates made the argument at the debate that the government forced mortgage lenders to make bad loans. But in reality, most subprime loans were made by companies that were not subject to any kind of federal regulation. Furthermore, there was no need to force anyone to make the loans.

How many subprime mortgages were there in 2006?Out of the top 25 subprime lenders in 2006, only one was subject to the usual mortgage laws and regulations. The nonbank underwriters made more than 12 million subprime mortgages with a value of nearly $2 trillion. The lenders who made these were exempt from federal regulations.

Article first time published onIs subprime lending ethical?

And the subprime mortgage business is indeed built on shaky ethical grounds. … Rather, the people who borrow on subprime rates have poorer credit and usually a higher history of credit defaults. Hence, they are willing to pay a premium, in the form of a higher interest rate and likely higher fees, for their mortgages.

Is FHA loan a subprime?

FHA loans are not subprime loans. However, since FHA loans are available to borrowers with less than perfect credit or low-income, many look at them the same. FHA home loans are actually a great deal for homebuyers. Such a good deal, in fact, that 46% of mortgage used by first-time homebuyers are FHA loans.

Does Canada have subprime mortgages?

In Canada, Subprime mortgages are openly available for all types of applicants. Subprime Mortgages are mortgages where the interest rate on the note is higher throughout the term of the loan.

Are subprime mortgages illegal?

Subprime mortgages are not illegal or even inherently bad. Subprime mortgages are simply mortgages granted to less qualified buyers, with low credit scores or uncertain income sources. But when originated in large numbers, they can be a danger to the housing market.

What is subprime rate?

Subprime rates are higher than average interest rates charged on loans to riskier borrowers. … The higher interest rate is intended to compensate for the greater degree of risk and higher likelihood of delinquency or default on these loans.

When did subprime mortgages start?

The subprime meltdown was the sharp increase in high-risk mortgages that went into default beginning in 2007, contributing to the most severe recession in decades. The housing boom of the mid-2000s—combined with low-interest rates at the time—prompted many lenders to offer home loans to individuals with poor credit.

What caused the crash of 2008?

The Great Recession, one of the worst economic declines in US history, officially lasted from December 2007 to June 2009. The collapse of the housing market — fueled by low interest rates, easy credit, insufficient regulation, and toxic subprime mortgages — led to the economic crisis.

Who went to jail for 2008 financial crisis?

Kareem SerageldinBorn1973 (age 47–48) Cairo, EgyptEducationYale University (1994)Known forThe only American to serve jail time as a result of the financial crisis of 2007–2008

When was the last housing bubble?

The last time the U.S. housing market looked this frothy was back in 2005 to 2007. Then home values crashed, with disastrous consequences. When the real estate bubble burst, the global economy plunged into the deepest downturn since the Great Depression.

Why were there so many foreclosures in 2008?

The foreclosure crisis is a result of multiple factors: mistakes by governmental agencies and predatory practices by lending institutions, unrealistic expectations by buyers that led to risky borrowing, and a collapse of a housing bubble that was further exacerbated by the worst economic downturn in decades.

Why do you think banks expanded their subprime lending so much in the mid 2000s?

This sudden increase in subprime mortgages was due in part to the Federal Reserve’s decision to significantly lower the Federal funds rate to spur growth.

Is Freddie Mac a Fannie Mae?

Though both enterprises are better known by their nicknames, Fannie Mae and Freddie Mac have more official titles: Fannie Mae is the Federal National Mortgage Association (FNMA) and Freddie Mac is the Federal Home Loan Mortgage Corporation (FMCC).

Who pushed subprime mortgages?

The GSEs had a pioneering role in expanding the use of subprime loans: In 1999, Franklin Raines first put Fannie Mae into subprimes, following up on earlier Fannie Mae efforts in the 1990s, which reduced mortgage down payment requirements.

Who is responsible for subprime mortgage crisis?

The Biggest Culprit: The Lenders Most of the blame is on the mortgage originators or the lenders. That’s because they were responsible for creating these problems. After all, the lenders were the ones who advanced loans to people with poor credit and a high risk of default. 7 Here’s why that happened.

Why did banks issue subprime loans?

Subprime borrowers are those who have poor credit histories and are therefore more likely to default. Lenders charge higher interest rates to provide more return for the greater risk. 5 So, that makes it too expensive for many subprime borrowers to make monthly payments.

Why did banks stop lending to each other?

Banks were beginning to experience liquidity problems as early as 2007 as they became increasingly unwilling to lend to each other due to rising default rates on sub- prime loans and uncertainty about each other’s exposure to these bad debts.

How do house prices affect banks?

Housing market is important from a macroprudential perspective because it has a strong effect on the banking sector. … According to the results (1) higher house prices lead to higher bank risk, (2) the higher the share of mortgage loans at a bank, the stronger the positive effect of house prices on bank risk.

Are adjustable rate mortgages subprime?

More often, subprime mortgage loans are adjustable rate mortgages (ARMs). A subprime mortgage is generally a loan that is meant to be offered to prospective borrowers with impaired credit records. The higher interest rate is intended to compensate the lender for accepting the greater risk in lending to such borrowers.

How much money did Goldman Sachs make off toxic CDOs in the first half of 2006?

Goldman-Sachs sold more than $3 billion worth of CDOs in the first half of 2006.

Are predatory loans illegal?

Legal Protections Federal laws protect consumers against predatory lenders. Chief among them is the Equal Credit Opportunity Act (ECOA). This law makes it illegal for a lender to impose a higher interest rate or higher fees based on a person’s race, color, religion, sex, age, marital status or national origin.

Why did banks believe that mortgage backed securities protected them from defaults?

Why did banks believe that mortgage-backed securities protected them from defaults? Multiple choice question. Home values were expected to continually rise. Loans within mortgage-backed securities had very low interest rates.